“The first rule of compounding: never interrupt it unnecessarily”

Charlie Munger

Predictions, it is said, are tough to make, especially when they are about the future.1 Yet the very business of investing concerns itself with prediction and its more official-sounding cousin, forecasting. Making predictions is unavoidable in investment management and since that is the case, the question then becomes how can one minimise the downside of negative outcomes associated with imperfect predictions? One way is to only make decisions when the level of certainty of outcome is high. Buying quality growth investments with structural drivers and durable competitive advantages is an example of this. We are significantly more certain of their investment merits than we are of the market as a whole. Another is simply to minimise the number of unnecessary predictions that one makes over the course of an investment. We believe that market timing is the main cause of such unnecessary predictions.

It is well established that the total returns of a stock follow the earnings growth of a business in the long term. This is something that we have discussed at length in the past. It is equally well established that share-price appreciation does not increase in a perfectly straight line. There are peaks and troughs where the market behaves more like Benjamin Graham’s short-term “voting machine” and less like his long-term “weighing machine”.2 Investors that try and profit from these ups and downs seek to be one step ahead of the market. They believe they will lose less (by pre-empting and positioning for downturns) and earn more (by pre-empting and positioning for upturns) than the average manager. In reality, they are merely introducing opportunities to interrupt the conversion of earnings into price appreciation, falling victim to recency bias and overreacting to near-term events.3 They often entirely ignore the fundamentals of the business (whose long-term characteristics often emerge from the crisis unchanged) and instead focus on forecasting market psychology, a practice that studies have shown is detrimental to returns.4

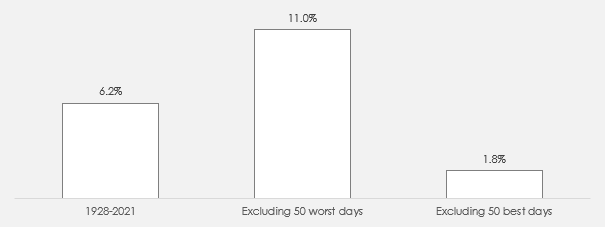

But how much can market timing mistakes punish the investor? Quite a lot it seems. If we take the compound annual growth rate of the S&P 500 Index from January 19285 until January 2021, we can see that it is a healthy 6.2 per cent. If an investor was able to time the market and avoid the worst 50 days, the returns would have increased to 11.0 per cent. Quite the result. However, if the investor had instead missed the 50 best days, the returns would have fallen to 1.8 per cent.

Figure 1: S&P 500 Index price returns

Source: Standard & Poor’s

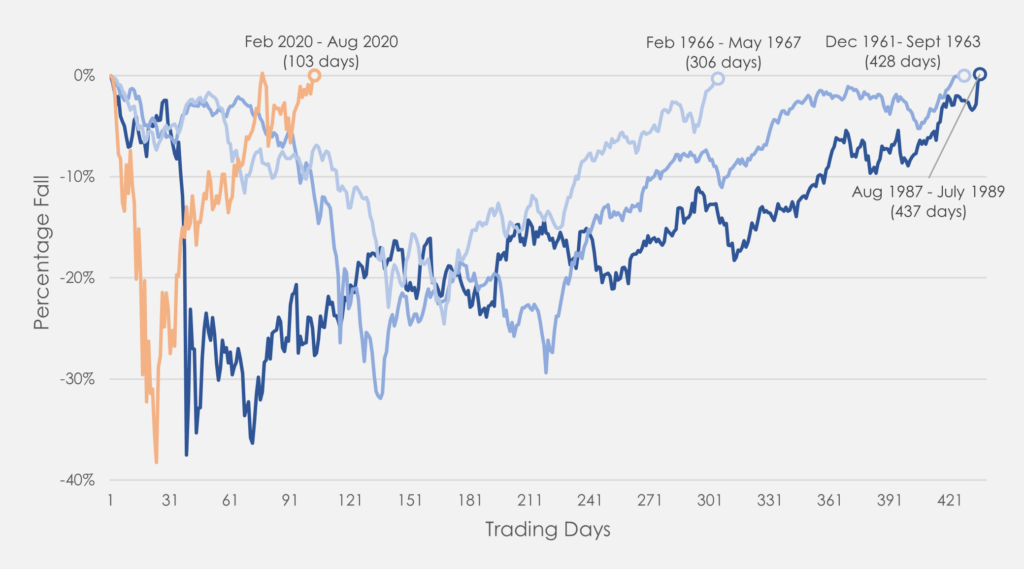

This finding has two major conclusions. First, that extreme events have a large bearing on investor returns and second, that the correct positioning prior to such extreme events would be helpful. But is it possible to successfully identify these extreme events and systematically capture the 50 best days while avoiding the 50 worst? The stock market seems to think not if volatility surrounding extreme events is any measure. The Covid-19 pandemic was a case in point, with the fastest stock market decline in history catching out those investors who were in the market, followed by the fastest recovery in history catching investors who sold.

Figure 2: Top Four S&P 500 Index Crashes & Recoveries

Source: Standard & Poor’s

Not only is it difficult to earn greater returns with market timing but academic research has also shown that it is detrimental to returns. Studies have suggested that there is a negative performance gap of between -0.05 per cent to -0.13 per cent per month for managers that time the market and managers that do not.6 If this is the case, there is little to gain and much to lose from market timing.

On the other hand, long-term buy-and-hold strategies benefit from both the continuous compounding of the business and any improvements in the risk profile of the investment. The long-term investor can afford to buy companies that would be too expensive for the short-term investor because the longer the stock is held, the more likely it is that the strong earnings will help it grow into the valuation.

As investors, our job is to try and find investments where the odds are in our favour. One of the tools that we use to tip those odds is our quality growth investment philosophy. This helps us find businesses that can grow sustainably over time. Another tool is our long-term holding strategy; once we find these securities that can compound earnings at attractive rates, we never interrupt this compounding unnecessarily.

MJ Faherty,

31st August, 2021

1A quote that is often attributed to author Mark Twain, philosophers Yogi Berra and Nos- tradamus, physicist Niels Bohr, poet Piet Hein and film producer Samuel Goldwyn (of Metro Goldwyn Mayer fame). As of 2007, the exact origin is unknown.

2Graham, B. The Intelligent Investor (1949).

3This topic has been extensively covered in academic literature, all stemming from the groundbreaking paper by De Bondt and Thaler (considered the father of behavioural economics). The authors found that investors showed a tendency to overweight recent information and underweight recent base rate data. De Bondt, W.F.M., and Thaler, R. H., (1985) “Does the Stock Market Overreact?” Journal of Finance, pp. 793-805.

4Bailey et al. found that behaviourally biased investors typically make poor decisions about fund style and expenses, trading frequency and timing, resulting in poor perfor- mance. Bailey, W., Kumar, A., & Ng, D. (2011). “Behavioral biases of mutual fund inves- tors”. Journal of Financial Economics, 102 (1), pp. 1-27.

5The index has data available from 3 January 1928.

6Using cash flows at an individual fund level, the author compared the dollar-weighted return with the time-weighted return and found a negative and statistically significant result for all funds under investigation. They came to the more damning conclusion that the “gaps remain negative regardless of the category of investment or the investment strategy declared by the fund manager”. Cagnazzo, Alberto, Market-Timing Performance of Mutual Fund Investors in Emerging Markets (April 10, 2020). Available at SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3364879

Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations. Nothing in this newsletter is a recommendation for a particular stock. The views, forecasts, opinions and or estimates and expectations expressed in this document are a reflection of Seilern Investment Management Ltd’s best judgment as of the date of this communication’s publication, and are subject to change. No responsibility or liability shall be accepted for amending, correcting, or updating any information or forecasts, opinions and or estimates and expectations contained herein.

Please be aware that past performance should not be seen as an indication of future performance. Any financial instrument included in this website could be considered high risk and investors may not get back all of their original investment. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and you may not receive back the amount originally invested. In addition stock market fluctuations and currency movements may also affect the value of investments.

Get the latest insights & events direct to your inbox

"*" indicates required fields