The volatility in markets so far this year has felt extreme with the S&P 500 already declining by -9.2 per cent at the time of writing and steep falls in high growth stocks and lockdown beneficiaries like Peloton that would impress even the cliff divers of Acapulco. While we would emphasise that we are more focussed on higher quality companies within the growth bucket- as Peter illustrates in his newsletter this month (The difference between Growth and Quality Growth) – we have certainly not escaped some similar treatment. While it is interesting to try and work out what is driving markets at any moment and how events may unfold, this has little bearing on how we invest. As we always say, we only do one thing: Quality Growth investing. To do this we simply look to find the best companies, those who can grow their earnings sustainably over the long term. We pick these companies precisely because they can weather all economic environments. And while their share prices may wax and wane with the trends and surprises that the global economy throws at them, the fundamentals of the businesses should persist. This means that over the long term, their share prices should prosper.

One of the biggest risks facing clients is their fund manager being tempted away from investing how they said they would, otherwise known as “style drift”. So, rather than looking ahead to the infinite possibilities of what might unfold over the next twelve months, instead I wanted to look back over the last ten years to see if we actually do as we say by assessing the consistency of our funds. As we wrote last month, it is important to hold onto quality growth companies, as over time good companies can see their earnings not only sustain, but in some cases accelerate. Yet there is more to running the funds than simply buying and holding. We must sell as well and indeed this can be a key component of outperformance.

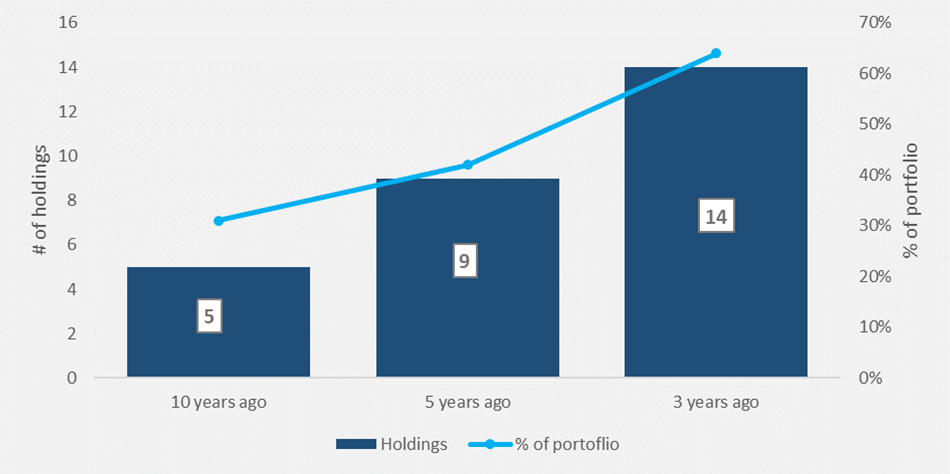

Casting your mind back exactly ten years ago to the beginning of 2012, it’s perhaps surprising to note how much has changed. Barack Obama was approaching the halfway point of his presidency; Boris Johnson was a popular Mayor of London, preparing for the city’s modern-day apogee of hosting the Olympics; Bitcoin had just endured a stratospheric crash from $30 to less than $5; and Novak Djokovic had successfully defended his Australian Open in Melbourne. The Seilern World Growth fund (SWG) meanwhile had the same two positions at the top of the fund as it does today: Alphabet and Mastercard. In fact, there were five companies in that portfolio that have remained in the fund all this time. These five positions accounted for 30 per cent of the portfolio back then and, today, they still account for 28 per cent demonstrating that our high conviction ideas have remained remarkably consistent. If we shorten the time horizon to five years, we find that nine companies have remained constant in the portfolio, accounting for just over 40 per cent of the fund’s weightings.

Figure 1: Number of companies still in SWG from 10, 5 and 3 years ago

This level of consistency is good going and is considerably ahead of most active fund managers, even those who claim they invest over the long term, for which they often really mean more than six months rather than six years.1

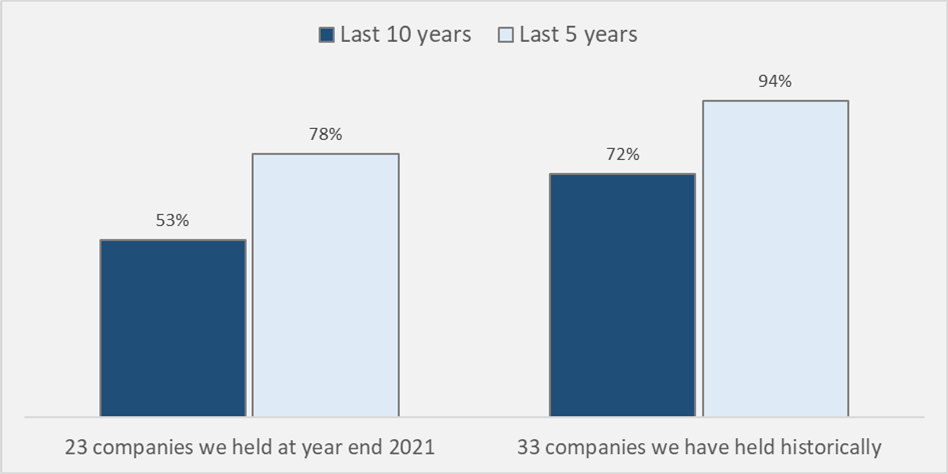

When we dig a bit closer though, we find that the fund has been even more consistent than this. If we look at the 23 positions we hold today, and track their historical weighting in the fund, we find that more than half of the fund’s overall weighting in the last 10 years has come from the positions we still hold today. Over the past five years, this rises to nearly three quarters of the fund’s current weighting. In fact we find that just 33 companies have been responsible for almost 80 per cent of the fund’s combined weighting over ten years, and 94 per cent over the past five years.

Figure 2: Portion of SWG’s historical weighting contributed by today’s positions

This consistency demonstrates our adherence to Seilern’s disciplined investment philosophy and process. It also shows we do not try and time markets by trading in and out of fashionable stocks. A good example of this was two years ago when Covid-19 was taking hold and market turmoil was starting to unfold. We held several long investment meetings and acknowledged that the fast-evolving pandemic could dramatically affect our companies and the wider global economy. Yet despite reaching this conclusion, after rigorous stress testing of all the Universe companies, when it came to the funds, we decided to do nothing. We select our companies precisely because they can survive tough times and thereby the impulse to trade is reduced.

However, while we often say that our philosophy is simple, it is not as simple as doing nothing. Ultimately there are three things that we need to do as investment managers:

1. Hold onto the companies that continue to generate earnings growth

2. Find new and interesting companies

3. Sell the companies that no longer meet our criteria

The first point is crucial in order to ensure we benefit fully from the compounding earnings power of our companies. As Marco pointed out in his last newsletter (Underestimating the Future), many of these companies experience increasing returns over time. We have the confidence to hold these companies through rocky times as we know that their competitive advantages and business models will hold over the long term.

This consistency is not the same thing as inertia. Long held faith in our longest held positions goes hand in hand with finding new and exciting businesses. Through our annual Search for Growth, we have added 17 new companies across our three strategies over the past five years. These are companies which we will hopefully hold on to over the next decade and have replaced the businesses that no longer meet our criteria.

Ideally, we would never have to sell a position. If a company continues to generate sustainable earnings growth, we will hold it indefinitely. Unfortunately, we don’t live in an ideal world. Some companies experience disruption as their competitive advantages get eroded away. For others, their markets reach full penetration and their industry growth drivers run out of steam. In both cases, earnings growth starts to slow. And from time to time, we find that our initial analysis has been incorrect and the company we thought was Quality Growth is in fact an impostor.

As well as being consistent we therefore need to be cold-blooded, acting decisively to cut companies before they have a chance to contaminate the funds with low growth and poor share performance. Again, we can see this ruthlessness in the numbers. For while 33 companies have been responsible for 80 per cent of the fund’s weighting over the past ten years, there have in been a further 29 companies that, at one point in time, were in the portfolio.

Hedge funds employ stop losses and similar strategies that offer a ‘shoot now, ask questions later’ strategy. In these cases, if one of their holdings falls more than 20 per cent, they will sell it, even if they do not know the reason for the fall. This makes sense for them as they often cover more than 100 positions. We use our in-depth analysis to continually assess whether our companies remain Quality Growth. As soon as we find a company that doesn’t meet our 10 Golden Rules, we sell it. It is not the share price that tells us when to sell, nor is performance our primary aim. The main purpose of selling a company is to preserve the quality of the fund, limiting it only to those companies that can still grow their earnings over the long term.

Over a prolonged period of time, however, this does often lead to improved performance. Returning to those 33 companies that have been responsible for 94 per cent of the fund’s weighting over the last five years, five that are no longer in the SWG fund are also no longer in the Seilern Universe. Since selling them from SWG, they have not cratered and have all seen positive returns. But they have lagged the performance of the fund by an average of –49.6 per cent.

As much as commentators and fund managers will always opine on how the year is going to unfold, no one knows what might be around the corner – as the last two years have so clearly shown. Trying to predict what will happen over five years or even the next decade is almost impossible. Rather than focussing on this, we instead concentrate on remaining consistent. To do so, we need to be highly active, continually assessing the worthiness of our companies. This enables us to carry on holding these companies through different market environments.

This reminds me of a familiar phrase used to describe Henry VIII’s advisor Sir Thomas More. He was known as ‘a man for all seasons’ because he always remained true to his principles under all circumstances. In the same way, our funds are ‘funds for all seasons’ because of their unwavering consistency. It is precisely because they remain the same and are of such a solid and firm structure, that they have stood the test of time.

1This has been shown in various studies over the years. In their paper “Patient Capital Outperformance The Investment Skill of High Active Share Managers Who Trade Infrequently” Cremers, M. and Ankur Pareek found the average holding period of US equity mutual funds had fallen to 1.4 years.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields