2022 will end up being an annus horribilis for an overwhelming portion of people across the globe. This is certainly true for investors across most asset classes, whose only comfort may be that at least their underperformance is comparable to other lacklustre years, unlike for the leaders of the UK’s Conservative party. While we dislike poor performance as much as anyone, performing over the short term where factors outside of our control can influence stock prices is not our priority. Our sights are set on a longer timeframe over which the likelihood increases that Stock prices will follow earnings growth With this in mind, it is consistency of style that we strive for, both in buoyant and in choppy markets, rather than consistency of performance. This style is Quality Growth, the core characteristic of which is sustainable earnings growth over time with strong returns on invested capital, something which we believe differentiates Quality Growth companies from the average company. All of our research efforts are focused on identifying and measuring this sustainable growth.

Because we hold companies that we expect to produce value for many years, we are aware that the vast majority of value-creation will not be created in the next one, two or five years, but in the years beyond that. When we measure the ability of a business to endure, we examine the effect that the underlying drivers of growth have on long-term cashflow generation. When we measure the risks that a business faces, we examine whether these risks affect its long-term cashflow generation. Our focus on the long term allows us to block out a lot of the noise that causes a near-term downgrade to earnings estimates but has scant impact on the structural drivers of the business. To put it differently, we must be able to differentiate between the risks and opportunities that have a temporary impact on the business today and the risks and opportunities that will have a structural impact on the business in the future.

Is it temporary or structural?

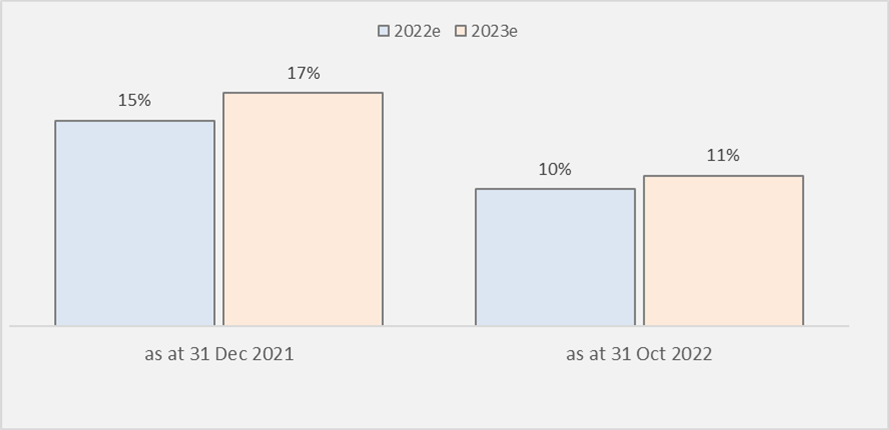

Throughout the course of this year, the anticipated level of Fiscal Year (FY) 2022 earnings for our companies has fallen. Whereas at the start of the year sell-side analysts were expecting the companies in the Seilern Universe to deliver 15 per cent earnings growth, they are now only forecasting 10 per cent growth. Put another way, the earnings expectations for our companies have fallen by -5 percentage points (Figure 1).

Figure 1: Changes in Universe Earnings Growth Expectations

Source: Bloomberg, Seilern Investment Management Ltd. as at 31 October 2022

While this is disappointing, it is not surprising. A war in Ukraine, soaring energy prices, ongoing Covid lockdowns, rising interest rates, and an exceptionally strong US Dollar are some of the unusual suspects this year. However, these disruptions have only had short-term effects on Quality Growth companies. There has been no impact on their ability to generate value into perpetuity, which is to say the level, duration and risks to cashflows have not materially changed. Indeed, it is worth reiterating that despite this negative macroeconomic backdrop and a very strong comparison period in 2021, we still expect the companies in the Seilern Universe to grow their earnings by an average of +10 per cent in FY2022, and by a few percentage points higher if we adjusted for the negative impacts of the rising US Dollar.

The range of factors that have impeded our companies this year, and specifically in the earnings season so far, fall under two broad categories: the aftershocks of Covid which are still working their way through the financial system; and the negative effects from a feared recession.

The spectre of Covid still hangs over us in many ways, some more obvious than others. In certain countries, most notably China, Covid lockdowns are ongoing. This has caused a decline in consumer confidence and demand that has stunted the growth of companies vying to sell products to Chinese consumers. These lockdowns also continue to disrupt supply chains, with the closure of factories leading to reduced supply of end products and leading to a shortage of key components, ranging from low-tech products such as running shoes to high-tech products such as semiconductors. Furthermore, Covid-induced supply chain disruptions lay at the heart of much of the rising inflation we saw in 2021. This has of course been exacerbated by the war in Ukraine and has led to rising costs, be it energy, wages or raw materials.

There are then the more tenuous repercussions from Covid. Some healthcare names are experiencing capacity issues because of a shortage of staff, many of whom are now taking time out of the industry after two years of long working hours and stress. Those suffering indirectly from staffing shortages include IDEXX Laboratories (veterinarians) and Edwards Lifesciences (hospital staff). Finally, many of our companies saw surging demand for their products and services during Covid, some of which was a pull forward of future demand. The bumper profits made in 2021 made it even harder for the likes of West Pharmaceutical Services, Google and Adobe to match those levels.

These Covid-related issues account for the majority of the earnings disappointments we have seen in our companies. While the media and markets are increasingly talking about an upcoming recession, this has not yet materialised in the numbers, with a few exceptions from the consumer discretionary sector. Some companies, however, have started to guide lower for next year, factoring in some negative demand due to economic uncertainty. In the likely event of a recession in 2023, we would certainly expect to see further downgrades for Quality Growth companies as demand falls or is pushed out into future years. However, thanks to their secular growth drivers and defensive characteristics, we believe that our companies are much better equipped to manage a fall in aggregate demand than the rest of the market. Furthermore, history tells us that the strong get stronger after periods of economic weakness as industries consolidate around the leaders.

As well as these two broad areas, many of our companies have also seen negative revisions due to the rising US Dollar, with US based exporters of goods and services being most affected here. Currency effects are not something we particularly worry about as it does not reflect the strength or weakness of our companies’ business models.

Lastly, there are certain discrete factors that have negatively impacted the earnings and share prices of single companies, such as delays in delivery of manufacturing equipment (West), large acquisitions (Adobe), one-off research and development investments (IDEXX), local bond market jitters (Rightmove) and the timing of customer contracts (Lonza). We do not believe that any of these will have a negative influence on the businesses in the long term, and in fact we believe that some of them will improve the long-term sustainability of their competitive advantages.

Ignoring the noise

Throughout the year, we have discussed how the largest driver of underperformance has been the speed and extent to which interest rates have risen, which have had a disproportionate impact on long-duration assets such as Quality Growth companies. This has weighed heavily upon their share prices. We have also discussed that underperformance has not been driven by structural weakness in our Universe companies; while some of our companies have seen their earnings revised down over the course of 2022, there has not been a single instance of revisions that relate to a change in a structural growth driver.

While we may (and expect to) see some further earnings downgrades across our Universe companies, we will measure these downgrades against our usual test – is the reason for the downgrade a temporary headwind or a structural decline? And when we eventually emerge from the downgrade cycle and enter the inevitable upgrade cycle that follows, we will apply the same test again. Our goal throughout is to maintain strict adherence to our Quality Growth philosophy, which has been the driver of our strong performance over time. This means that when prices fall but fundamentals remain strong, we register an improvement in future returns and an opportunity to purchase Quality Growth companies at rare discounts.

Q. Macfarlane & MJ. Faherty,

31st October, 2022

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields