Quality Growth businesses are often described as the quintessential long-duration asset. In 2022, interest rates rose rapidly and unexpectedly from a very low base. Inasmuch as rising interest rates lessen the present value of future cash flow streams, there is a general view that Quality Growth companies are most at risk in this environment.

Two questions we have received from investors are whether the performance of our companies last year was justified, and what happens to the premium of Quality Growth businesses if rates stay “higher for longer”?

To us, the answer to these questions offer several key observations. First, price is not always the same as value and these can become dislocated in the short term. Secondly, what affects Quality Growth investments in the short term is not necessarily how high rates are, but their direction and magnitude of change. Over the long term, we believe that earnings drive share prices; we value those earnings using a discounted cash flow model, and so the mathematical relationship between discounting a far-in-the-future stream of cash flows at a rate that is suddenly significantly higher than zero means this value can compress, sometimes significantly. But the value of our businesses does not lie in the next few years’ earnings, it lies in the perpetuity. Our focus is therefore on ensuring that our companies’ ability to generate sustainable cash flows over a long period of time is not affected. Provided they can do this above the cost of capital, we believe that Quality Growth businesses ought to continue to command a premium valuation relative to other assets.

In this newsletter we explore these conclusions further.

The concept of equity duration

Since the value of every financial asset is ultimately a function of its future cash flows, duration gives investors a window into the price sensitivity of an asset to changes in interest rates.

The concept of duration is well understood in the context of fixed income securities. With bonds, you know exactly what the bond will pay in interest each period until maturity, so you can mathematically calculate its duration and thus its sensitivity to interest rates.

With equities, it’s more complicated. Taking the analogy to fixed income, one way to think about this is how long (in years) an investor must receive distributable cash flows in order to be repaid the purchase price of the stock. The challenge is that we don’t know with precision how much distributable cash flow a company will generate over the next 10 years and beyond. Management teams broadly have two choices, they can reinvest the cash flows into the business (our preferred option when they can do so at higher internal rates of return because the company has attractive growth prospects) or return capital to shareholders via dividends and share buybacks. Another way, and how we think about equity duration, is not necessarily the distributable cash flows but rather the company’s ability to generate cash flows over the very long term; because we believe that earnings drive share prices, the “distributable cash flows” comes in the form of the capital appreciation as the stock price reflects this over time. Under either approach, the uncertainty in terms of both the level of (distributable) cash flows and the time it takes to receive them increases a stock’s duration (in other words, its sensitivity to changes in interest rates). Moreover, unlike bonds, there is no maturity date on businesses.

In this sense, equities are inherently long-duration assets, and within that, there are shorter- and longer-duration stocks.

Short- and long-duration companies

A stock can therefore be thought of as analogous to a perpetual, zero coupon bond (ZCB). In the case of a ZCB, all the cash flows come much later in its life cycle; the same can be said for long-duration equities.

In the case of Quality Growth companies, these have long-term, structural growth drivers, meaning the value of the business is not in the cash flows it will generate in the next one, two or three years, but rather the bulk of the company’s value comes from the cash flows it is able to generate after year five (and ideally, into perpetuity). Indeed, for the average Seilern Universe company, over 85 per cent of its total value comes from these longer dated cash flows. A Quality Growth company can achieve this sustained growth in a number of ways including by establishing powerful network effects, providing mission-critical non-core products or services to its customer (Searching for the (non) core), achieving scale through structural cost advantages, or building a wide moat from the quality and reputation of its brand. These companies can consistently out earn their cost of capital and compound those returns over many years, rather than for brief, cyclical periods. Moreover, because Quality Growth companies are self-funding, the cost of capital is not so much of an issue for them; they also generally have low debt so servicing costs are also not an issue when rates rise.1

A short-duration stock on the other hand, can be thought of as a company that may be generating cash flow today but with low- to no- long-term terminal value; it is therefore returning capital to shareholders via higher dividends and stock repurchases because it lacks attractive options to reinvest its cash flows internally at rates of return greater than its cost of capital. As a generalisation, these tend to be cyclical companies in sectors that we avoid because they lack long-term secular growth drivers (The Power Of Exclusion).

We can further explore this distinction by looking at two fictional companies, one long-duration and the other short-duration, each with $100 in free cash flow today.

Figure 1: Long-duration and short-duration company assumptions

Source: Seilern Investment Management, 2023

The long-duration company is growing its annual cash flows at 10 per cent, which is in line with the long term growth rate of the Seilern Universe, and has a perpetual growth rate of 3 per cent. A short-duration company could be expected to grow, through the cycle, in line with global GDP, at around 2.5 per cent, and to have a perpetual growth rate in line with that. Naturally, the perpetual growth rate of our Universe companies should be higher than the broader market given that the secular growth drivers behind our businesses are stronger.

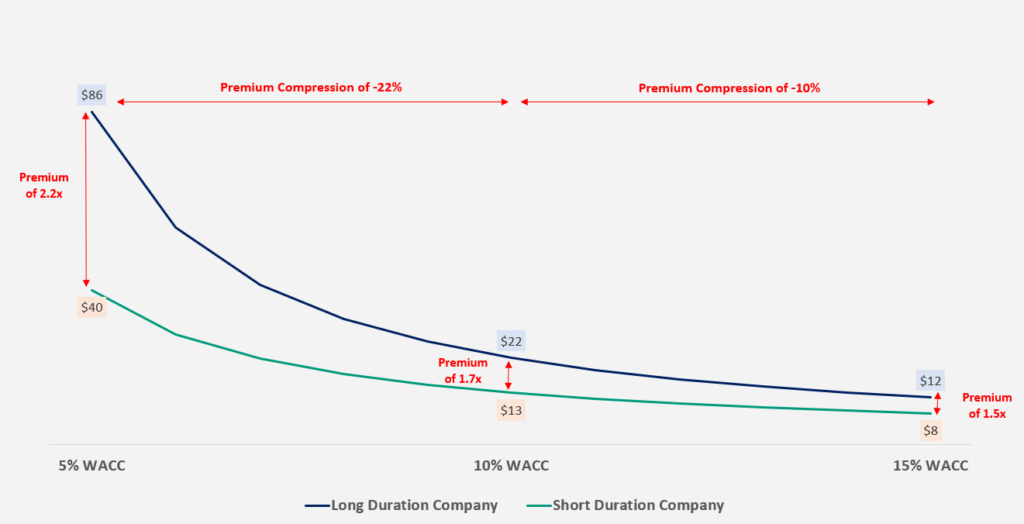

Based on these assumptions, we can simulate how the valuation of these two companies changes in different interest rate environments, proxied by changes in the weighted average cost of capital (the WACC). As the following chart shows, the long-duration company’s fair value is more sensitive to changes in the discount rate.

Figure 2: Company valuations at different WACC rates

Source: Seilern Investment Management, 2023

If we distil the valuation differential into a premium, in the 5 per cent rate environment you would be paying 2.2x more for the long-duration asset than the short-duration asset. As rates rise from 5 per cent to 10 per cent, the premium compresses by -22 per cent; this is similar to the dynamic we saw play out in 2022, as the US 10-year yield more than doubled and the share prices of Quality Growth companies fell. However, in the second stage where rates increase from 10 per cent to 15 per cent, the premium compression is meaningfully less, only -10 per cent in theory.

From this, there are several conclusions we can draw. Firstly, the lower the long-term bond yield (ie the starting point at the beginning of 2022) the more sensitive the value of the long-duration company becomes to changing discount rates. This is because the present-day value of future cash flows (especially the terminal value) is magnified when the discounting calculation is based on a very low interest rate. Secondly, the change in yields from this lower base (for example, from 0 per cent to 5 per cent) will have a larger impact on the valuation than when yields rise from an already higher starting point (for example, from 5 per cent to 10 per cent). As a result, the premium for an asset with longer dated cash flows will compress by less as discount rates rise. Ultimately, long-duration assets only deserve this premium if they can generate a strong and stable level of growth, which can then be sustained for long periods of time.

The last point is perhaps the most important. Most of the value of a long-duration company lies in its terminal value and a key determinant of that value is the durability of its perpetual growth rate. This, in turn, is directly related to the long-term secular growth drivers of the industry it operates in, the consistency of the company’s leadership within that industry, its competitive positioning, the scalability of its business model and its ability to generate organic growth, the first five of our Golden Rules. Forecasting inevitably involves assumptions, but investors who have the luxury of time to thoroughly research companies drastically increase their odds of forecasting with any degree of accuracy (Underestimating the Future). That is why we do so much in-depth, qualitative analysis on our companies so that we can properly assess whether their perpetual growth rates have a higher likelihood of being durable in the very long term.

A case study: ANSYS, Inc.

So much for the theory, what happens in practice? ANSYS, a company that has been in the Seilern Universe since December 2012, provides an interesting case study.

ANSYS creates simulation software for engineering applications. Its software enables engineers to simulate product behaviour in a virtual environment prior to being built or deployed in the real world. For example, using ANSYS’ software, engineers can create a virtual model of the braking system for a car and simulate how it will perform under different conditions, such as different speeds, road conditions and temperatures. They can also analyse how different materials and designs will affect the system’s performance, such as the brake pads and rotors. By testing and optimising the design in a virtual environment, it reduces the need for physical prototypes and testing, which saves time and resources and improves product safety.

ANSYS’ products are not just sold into the automotive sector, they are also ubiquitous in the aerospace, defence, energy, healthcare and electronics industries. As a result, its total addressable market is large and growing as more users across the product validation chain use ANSYS’ software to simulate more and more products that require more complex, multi-physics computations. The expansion of ANSYS’ products to new and emerging use cases is being driven by secular growth trends such as electrification, autonomy, connectivity, the industrial internet-of-things and sustainability.

ANSYS is therefore one of the longest-duration companies in our Universe. Even though it is very profitable today and expected to grow its free cash flows at a CAGR of 12 per cent over the next 10 years,2 we estimate that the majority of its value resides in the cash flows it will generate beyond this; this increases its sensitivity to changes in interest rates, as can be seen in the following chart which plots ANSYS’ share price performance against its earning per share growth since the start of 2018.3

Figure 3: ANSYS – Share price performance vs EPS return (indexed to 31 December 2017)

Source: FactSet, Seilern Investment Management, 2023

To describe the four stages in this chart, [1] around this time ANSYS’ earnings began to inflect; following a leadership transition it began to sign a number of record new deals and saw a shift in customer preference from perpetual licences to a term-based leasing model which improved its recurring revenues. [2] During Covid, ANSYS enjoyed strong share price performance,4arguably not fundamentally driven but due to the precipitous fall in interest rates and abundant liquidity in financial markets. Yet its earnings were also defensive; they didn’t collapse as countries locked down but growth looking forward was difficult because the capex budgets for companies wanting to buy its simulation software were paused. We had high conviction that this challenging demand picture would improve, and so having a long-term view and the time to analyse our businesses in depth gives us the ability during tough times to make long-term decisions. [3] As the demand picture improved throughout 2022, ANSYS saw earnings upgrades of 8 per cent, however its share price fell 40 per cent. Why – because interest rates rose sharply from a low base and as a long-duration asset its valuation is highly influenced by changes in long-term yields. [4] Thus far in 2023 we have started to see the market differentiate between those long-duration companies which are purely benefiting from the macroeconomic environment, and those which are also underpinned by strong fundamentals. Over the last five years, ANSYS’ earnings and share price have grown broadly in line at a CAGR of around 15 per cent,5 so over longer timeframes the relationship between earnings and share prices does exist but it can break down over shorter periods (although we would caution that five years is still a relatively short timeframe during which prices can still decorrelate from fundamentals).

Conclusion

Attempting to analyse the mechanical relationship between company valuations and changes in interest rates is simplistic at best, and misleading at worst. For one, it doesn’t take into account other variables such as changes in nominal cash flows and perpetual growth rates as discount rates move. As a result, the relationship may be weaker or even go against the natural first instinct, depending on the circumstances.

Despite these shortcomings, we believe it can still provide a useful framework. At the end of 2021, Quality Growth companies were trading on a significant premium to the market; arguably, this was justifiable given the superior characteristics of Quality Growth companies and the market’s extrapolation that the near-zero interest environment would continue. So, a lot of the pain we saw in 2022 was in some respects inevitable given the sheer velocity of changes in rates.

Having spent a lot of time last year re-assessing how each of our companies would fare should inflation remain higher for longer or we enter a recession, we are comfortable that their ability to continue to generate strong and sustainable cash flows over the long term is not affected, and this is where their value lies. Going forward, the relative changes in discount rates should have a lesser effect on the long-term value of our businesses; and their enduring characteristics mean that they should justifiably continue to command a premium valuation relative to the wider market.

C. Hoelzl,

31st July 2023

1Interestingly on this topic, we did not change our discount rate when interest rates fell, nor did we increase it when interest rates rose. Instead, we use a very long-term average rate of 3.5 per cent in the WACC in our discounted cash flow valuation and we use a WACC of around 7.5 per cent for all our Universe companies.

2Based on Seilern estimates.

3ANSYS’ share price and non-GAAP EPS excluding stock option expense, 31 December 2017 – 30 June 2023.

4Rising +72.5 per cent between March 2020 and December 2021.

5ANSYS’ share price and non-GAAP EPS excluding stock option expense, 31 December 2017 – 30 June 2023.

Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations. Nothing in this newsletter is a recommendation for a particular stock. The views, forecasts, opinions and or estimates and expectations expressed in this document are a reflection of Seilern Investment Management Ltd’s best judgment as of the date of this communication’s publication, and are subject to change. No responsibility or liability shall be accepted for amending, correcting, or updating any information or forecasts, opinions and or estimates and expectations contained herein.

Please be aware that past performance should not be seen as an indication of future performance. Any financial instrument included in this website could be considered high risk and investors may not get back all of their original investment. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and you may not receive back the amount originally invested. In addition stock market fluctuations and currency movements may also affect the value of investments.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields